This page is based on the chapter

“Timeseries”

of the Modern Polars book.

Preparing Data

Since the PRQL and SQL results shown on this page are after being

converted to R DataFrame via knitr, they have been converted from DuckDB

types to R types. So NULL in DuckDB is shown as NA.

Download

Download the data from Binance REST

API

and write it to a Parquet file.

This document uses R to download the data from the source here, but we

can also download and use the Parquet file included in the

kevinheavey/modern-polars

GitHub repository.

Code

R

data_path <- "data/ohlcv.parquet"

if (!fs::file_exists(data_path)) {

fs::dir_create(fs::path_dir(data_path))

.epoch_ms <- function(dt) {

dt |>

lubridate::as_datetime() |>

(\(x) (as.integer(x) * 1000))()

}

.start <- lubridate::make_datetime(2021, 1, 1) |> .epoch_ms()

.end <- lubridate::make_datetime(2022, 1, 1) |> .epoch_ms()

.url <- glue::glue(

"https://api.binance.com/api/v3/klines?symbol=BTCUSDT&",

"interval=1d&startTime={.start}&endTime={.end}"

)

.res <- jsonlite::read_json(.url)

time_col <- "time"

ohlcv_cols <- c(

"open",

"high",

"low",

"close",

"volume"

)

cols_to_use <- c(time_col, ohlcv_cols)

cols <- c(cols_to_use, glue::glue("ignore_{i}", i = 1:6))

df <- .res |>

tibble::enframe(name = NULL) |>

tidyr::unnest_wider(value, names_sep = "_") |>

rlang::set_names({{ cols }}) |>

dplyr::mutate(

dplyr::across({{ time_col }}, \(x) lubridate::as_datetime(x / 1000) |> lubridate::as_date()),

dplyr::across({{ ohlcv_cols }}, as.numeric),

.keep = "none"

)

con_tmp <- DBI::dbConnect(duckdb::duckdb(), ":memory:")

duckdb::duckdb_register(con_tmp, "df", df)

duckdb:::sql(glue::glue("COPY df TO '{data_path}' (FORMAT PARQUET)"), con_tmp)

DBI::dbDisconnect(con_tmp)

}

This is a sample command to download the Parquet file from the

kevinheavey/modern-polars GitHub repository.

Terminal

mkdir data

curl -sL https://github.com/kevinheavey/modern-polars/raw/d67d6f95ce0de8aad5492c4497ac4c3e33d696e8/data/ohlcv.pq -o data/ohlcv.parquet

Load the Data

After the Parquet file is ready, load that into DuckDB (in-memory)

database table, R DataFrame, and Python polars.LazyFrame.

- DuckDB

- R DataFrame

- Python polars.LazyFrame

SQL

CREATE TABLE tab AS FROM 'data/ohlcv.parquet'

| 2021-01-01 |

28923.63 |

29600.00 |

28624.57 |

29331.69 |

54182.93 |

| 2021-01-02 |

29331.70 |

33300.00 |

28946.53 |

32178.33 |

129993.87 |

| 2021-01-03 |

32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.57 |

| 2021-01-04 |

33000.05 |

33600.00 |

28130.00 |

31988.71 |

140899.89 |

| 2021-01-05 |

31989.75 |

34360.00 |

29900.00 |

33949.53 |

116050.00 |

R

library(dplyr, warn.conflicts = FALSE)

df <- duckdb:::sql("FROM 'data/ohlcv.parquet'")

| 2021-01-01 |

28923.63 |

29600.00 |

28624.57 |

29331.69 |

54182.93 |

| 2021-01-02 |

29331.70 |

33300.00 |

28946.53 |

32178.33 |

129993.87 |

| 2021-01-03 |

32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.57 |

| 2021-01-04 |

33000.05 |

33600.00 |

28130.00 |

31988.71 |

140899.89 |

| 2021-01-05 |

31989.75 |

34360.00 |

29900.00 |

33949.53 |

116050.00 |

Python

import polars as pl

lf = pl.scan_parquet("data/ohlcv.parquet")

shape: (5, 6)

| date |

f64 |

f64 |

f64 |

f64 |

f64 |

| 2021-01-01 |

28923.63 |

29600.0 |

28624.57 |

29331.69 |

54182.925011 |

| 2021-01-02 |

29331.7 |

33300.0 |

28946.53 |

32178.33 |

129993.873362 |

| 2021-01-03 |

32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.56675 |

| 2021-01-04 |

33000.05 |

33600.0 |

28130.0 |

31988.71 |

140899.88569 |

| 2021-01-05 |

31989.75 |

34360.0 |

29900.0 |

33949.53 |

116049.997038 |

Filtering

- PRQL DuckDB

- SQL DuckDB

- dplyr R

- Python Polars

PRQL

from tab

filter s"date_part(['year', 'month'], time) = {{year: 2021, month: 2}}"

take 5

| 2021-02-01 |

33092.97 |

34717.27 |

32296.16 |

33526.37 |

82718.28 |

| 2021-02-02 |

33517.09 |

35984.33 |

33418.00 |

35466.24 |

78056.66 |

| 2021-02-03 |

35472.71 |

37662.63 |

35362.38 |

37618.87 |

80784.33 |

| 2021-02-04 |

37620.26 |

38708.27 |

36161.95 |

36936.66 |

92080.74 |

| 2021-02-05 |

36936.65 |

38310.12 |

36570.00 |

38290.24 |

66681.33 |

SQL

FROM tab

WHERE date_part(['year', 'month'], time) = {year: 2021, month: 2}

LIMIT 5

| 2021-02-01 |

33092.97 |

34717.27 |

32296.16 |

33526.37 |

82718.28 |

| 2021-02-02 |

33517.09 |

35984.33 |

33418.00 |

35466.24 |

78056.66 |

| 2021-02-03 |

35472.71 |

37662.63 |

35362.38 |

37618.87 |

80784.33 |

| 2021-02-04 |

37620.26 |

38708.27 |

36161.95 |

36936.66 |

92080.74 |

| 2021-02-05 |

36936.65 |

38310.12 |

36570.00 |

38290.24 |

66681.33 |

R

df |>

filter(

lubridate::floor_date(time, "month") == lubridate::make_datetime(2021, 2)

) |>

head(5)

| 2021-02-01 |

33092.97 |

34717.27 |

32296.16 |

33526.37 |

82718.28 |

| 2021-02-02 |

33517.09 |

35984.33 |

33418.00 |

35466.24 |

78056.66 |

| 2021-02-03 |

35472.71 |

37662.63 |

35362.38 |

37618.87 |

80784.33 |

| 2021-02-04 |

37620.26 |

38708.27 |

36161.95 |

36936.66 |

92080.74 |

| 2021-02-05 |

36936.65 |

38310.12 |

36570.00 |

38290.24 |

66681.33 |

Python

(

lf.filter((pl.col("time").dt.year() == 2021) & (pl.col("time").dt.month() == 2))

.head(5)

.collect()

)

shape: (5, 6)

| date |

f64 |

f64 |

f64 |

f64 |

f64 |

| 2021-02-01 |

33092.97 |

34717.27 |

32296.16 |

33526.37 |

82718.276882 |

| 2021-02-02 |

33517.09 |

35984.33 |

33418.0 |

35466.24 |

78056.65988 |

| 2021-02-03 |

35472.71 |

37662.63 |

35362.38 |

37618.87 |

80784.333663 |

| 2021-02-04 |

37620.26 |

38708.27 |

36161.95 |

36936.66 |

92080.735898 |

| 2021-02-05 |

36936.65 |

38310.12 |

36570.0 |

38290.24 |

66681.334275 |

Downsampling

It is important to note carefully how units such as 5 days or 1 week

actually work. In other words, where to start counting 5 days or

1 week could be completely different in each system.

Here, we should note that time_bucket in DuckDB,

lubridate::floor_date in R, and group_by_dynamic in Polars have

completely different initial starting points by default.

-

The DuckDB function time_bucket’s origin defaults to

2000-01-03 00:00:00+00 for days or weeks interval.1

-

In the R lubridate::floor_date function, timestamp is floored

using the number of days elapsed since the beginning of every month

when specifying "5 days" to the unit argument.

R

lubridate::as_date(c("2023-01-31", "2023-02-01")) |>

lubridate::floor_date("5 days")

[1] "2023-01-31" "2023-02-01"

And when "1 week" to the unit argument, it is floored to the

nearest week, Sunday through Saturday.

R

lubridate::as_date(c("2023-01-31", "2023-02-01")) |>

lubridate::floor_date("1 week")

[1] "2023-01-29" "2023-01-29"

To start from an arbitrary origin, all breaks must be specified as a

vector in the unit argument.2

R

lubridate::as_date(c("2023-01-31", "2023-02-01")) |>

lubridate::floor_date(lubridate::make_date(2023, 1, 31))

[1] "2023-01-31" "2023-01-31"

-

group_by_dynamic of Polars, the offset parameter to specify the

origin point, is negative every by default.3

- PRQL DuckDB

- SQL DuckDB

- dplyr R

- Python Polars

PRQL

from tab

derive {

time_new = s"""

time_bucket(INTERVAL '5 days', time, (FROM tab SELECT min(time)))

"""

}

group {time_new} (

aggregate {

open = average open,

high = average high,

low = average low,

close = average close,

volume = average volume

}

)

sort time_new

take 5

| 2021-01-01 |

31084.32 |

33127.62 |

29512.82 |

32089.66 |

112416.85 |

| 2021-01-06 |

38165.31 |

40396.84 |

35983.82 |

39004.54 |

118750.08 |

| 2021-01-11 |

36825.23 |

38518.10 |

33288.05 |

36542.76 |

146166.70 |

| 2021-01-16 |

36216.36 |

37307.53 |

34650.37 |

35962.92 |

81236.80 |

| 2021-01-21 |

32721.53 |

34165.71 |

30624.23 |

32077.48 |

97809.66 |

SQL

WITH _tab1 AS (

FROM tab

SELECT

* REPLACE (time_bucket(INTERVAL '5 days', time, (FROM tab SELECT min(time)))) AS time

)

FROM _tab1

SELECT

time,

avg(COLUMNS(x -> x NOT IN ('time')))

GROUP BY time

ORDER BY time

LIMIT 5

| 2021-01-01 |

31084.32 |

33127.62 |

29512.82 |

32089.66 |

112416.85 |

| 2021-01-06 |

38165.31 |

40396.84 |

35983.82 |

39004.54 |

118750.08 |

| 2021-01-11 |

36825.23 |

38518.10 |

33288.05 |

36542.76 |

146166.70 |

| 2021-01-16 |

36216.36 |

37307.53 |

34650.37 |

35962.92 |

81236.80 |

| 2021-01-21 |

32721.53 |

34165.71 |

30624.23 |

32077.48 |

97809.66 |

R

df |>

mutate(

time = time |>

(\(x) lubridate::floor_date(x, seq(min(x), max(x), by = 5)))()

) |>

summarise(across(everything(), mean), .by = time) |>

head(5)

| 2021-01-01 |

31084.32 |

33127.62 |

29512.82 |

32089.66 |

112416.85 |

| 2021-01-06 |

38165.31 |

40396.84 |

35983.82 |

39004.54 |

118750.08 |

| 2021-01-11 |

36825.23 |

38518.10 |

33288.05 |

36542.76 |

146166.70 |

| 2021-01-16 |

36216.36 |

37307.53 |

34650.37 |

35962.92 |

81236.80 |

| 2021-01-21 |

32721.53 |

34165.71 |

30624.23 |

32077.48 |

97809.66 |

Python

(

lf.sort("time")

.group_by_dynamic("time", every="5d")

.agg(pl.col(pl.Float64).mean())

.head(5)

.collect()

)

shape: (5, 6)

| date |

f64 |

f64 |

f64 |

f64 |

f64 |

| 2020-12-29 |

29127.665 |

31450.0 |

28785.55 |

30755.01 |

92088.399186 |

| 2021-01-03 |

33577.028 |

36008.464 |

31916.198 |

35027.986 |

127574.470245 |

| 2021-01-08 |

38733.61 |

39914.548 |

34656.422 |

37655.352 |

143777.954392 |

| 2021-01-13 |

36659.63 |

38500.052 |

34539.406 |

37016.338 |

102447.076833 |

| 2021-01-18 |

34933.922 |

36232.334 |

32593.012 |

34357.258 |

103530.722029 |

- PRQL DuckDB

- SQL DukcDB

- dplyr R

- Python Polars

PRQL

from tab

derive {

time_new = s"""

time_bucket(INTERVAL '7 days', time, (FROM tab SELECT min(time)))

"""

}

group {time_new} (

aggregate {

open_mean = average open,

high_mean = average high,

low_mean = average low,

close_mean = average close,

volume_mean = average volume,

open_sum = sum open,

high_sum = sum high,

low_sum = sum low,

close_sum = sum close,

volume_sum = sum volume

}

)

sort time_new

take 5

| 2021-01-01 |

32305.78 |

34706.05 |

31021.73 |

33807.14 |

117435.59 |

226140.5 |

242942.3 |

217152.1 |

236650.0 |

822049.1 |

| 2021-01-08 |

37869.80 |

39646.11 |

34623.33 |

37827.52 |

135188.30 |

265088.6 |

277522.7 |

242363.3 |

264792.6 |

946318.1 |

| 2021-01-15 |

36527.89 |

37412.20 |

33961.55 |

35343.85 |

94212.72 |

255695.2 |

261885.4 |

237730.9 |

247406.9 |

659489.0 |

| 2021-01-22 |

31888.55 |

33498.81 |

30424.48 |

32248.01 |

89649.94 |

223219.8 |

234491.7 |

212971.4 |

225736.0 |

627549.6 |

| 2021-01-29 |

34511.48 |

36411.44 |

33450.08 |

35022.31 |

102728.42 |

241580.4 |

254880.1 |

234150.6 |

245156.2 |

719099.0 |

SQL

WITH _tab1 AS (

FROM tab

SELECT

* REPLACE (time_bucket(INTERVAL '7 days', time, (FROM tab SELECT min(time)))) AS time

)

FROM _tab1

SELECT

time,

avg(COLUMNS(x -> x NOT IN ('time'))),

sum(COLUMNS(x -> x NOT IN ('time')))

GROUP BY time

ORDER BY time

LIMIT 5

| 2021-01-01 |

32305.78 |

34706.05 |

31021.73 |

33807.14 |

117435.59 |

226140.5 |

242942.3 |

217152.1 |

236650.0 |

822049.1 |

| 2021-01-08 |

37869.80 |

39646.11 |

34623.33 |

37827.52 |

135188.30 |

265088.6 |

277522.7 |

242363.3 |

264792.6 |

946318.1 |

| 2021-01-15 |

36527.89 |

37412.20 |

33961.55 |

35343.85 |

94212.72 |

255695.2 |

261885.4 |

237730.9 |

247406.9 |

659489.0 |

| 2021-01-22 |

31888.55 |

33498.81 |

30424.48 |

32248.01 |

89649.94 |

223219.8 |

234491.7 |

212971.4 |

225736.0 |

627549.6 |

| 2021-01-29 |

34511.48 |

36411.44 |

33450.08 |

35022.31 |

102728.42 |

241580.4 |

254880.1 |

234150.6 |

245156.2 |

719099.0 |

R

df |>

mutate(

time = time |>

(\(x) lubridate::floor_date(x, seq(min(x), max(x), by = 7)))()

) |>

summarise(

across(

everything(),

list(mean = mean, sum = sum),

.names = "{.col}_{.fn}"

),

.by = time

) |>

head(5)

| 2021-01-01 |

32305.78 |

226140.5 |

34706.05 |

242942.3 |

31021.73 |

217152.1 |

33807.14 |

236650.0 |

117435.59 |

822049.1 |

| 2021-01-08 |

37869.80 |

265088.6 |

39646.11 |

277522.7 |

34623.33 |

242363.3 |

37827.52 |

264792.6 |

135188.30 |

946318.1 |

| 2021-01-15 |

36527.89 |

255695.2 |

37412.20 |

261885.4 |

33961.55 |

237730.9 |

35343.85 |

247406.9 |

94212.72 |

659489.0 |

| 2021-01-22 |

31888.55 |

223219.8 |

33498.81 |

234491.7 |

30424.48 |

212971.4 |

32248.01 |

225736.0 |

89649.94 |

627549.6 |

| 2021-01-29 |

34511.48 |

241580.4 |

36411.44 |

254880.1 |

33450.08 |

234150.6 |

35022.31 |

245156.2 |

102728.42 |

719099.0 |

Python

(

lf.sort("time")

.group_by_dynamic("time", every="1w")

.agg(

[

pl.col(pl.Float64).mean().name.suffix("_mean"),

pl.col(pl.Float64).sum().name.suffix("_sum"),

]

)

.head(5)

.collect()

)

shape: (5, 11)

| date |

f64 |

f64 |

f64 |

f64 |

f64 |

f64 |

f64 |

f64 |

f64 |

f64 |

| 2020-12-28 |

30143.926667 |

32559.37 |

29844.696667 |

31503.356667 |

101711.455041 |

90431.78 |

97678.11 |

89534.09 |

94510.07 |

305134.365123 |

| 2021-01-04 |

36545.192857 |

38563.458571 |

33992.73 |

37280.132857 |

121528.60945 |

255816.35 |

269944.21 |

237949.11 |

260960.93 |

850700.266152 |

| 2021-01-11 |

36694.077143 |

38199.0 |

33664.004286 |

36362.485714 |

128191.382064 |

256858.54 |

267393.0 |

235648.03 |

254537.4 |

897339.67445 |

| 2021-01-18 |

34242.515714 |

35384.095714 |

32179.317143 |

33732.027143 |

91460.990826 |

239697.61 |

247688.67 |

225255.22 |

236124.19 |

640226.935785 |

| 2021-01-25 |

32745.312857 |

34563.677143 |

31249.037143 |

32865.862857 |

106780.501216 |

229217.19 |

241945.74 |

218743.26 |

230061.04 |

747463.508509 |

Upsampling

The way to use a function like generate_series to generate sequential

values and then join them is general-purpose.

In R, we can also use dedicated functions like

timetk::pad_by_time.

- PRQL DuckDB

- SQL DuckDB

- dplyr R

- Python Polars

This example does not work with prql-compiler 0.11.1.

(PRQL/prql#3129)

PRQL

let _tab1 = s"""

SELECT

generate_series(

(SELECT min(time)),

(SELECT max(time)),

INTERVAL '6 hours'

).unnest() AS time

FROM tab

"""

from _tab1

join side:left tab (==time)

sort tab.time

select !{tab.time}

take 5

SQL

WITH _tab1 AS (

SELECT

generate_series(

(FROM tab SELECT min(time)),

(FROM tab SELECT max(time)),

INTERVAL '6 hours'

).unnest() AS time

)

FROM _tab1

LEFT JOIN tab USING (time)

ORDER BY time

LIMIT 5

| 2021-01-01 00:00:00 |

28923.63 |

29600 |

28624.57 |

29331.69 |

54182.93 |

| 2021-01-01 06:00:00 |

NA |

NA |

NA |

NA |

NA |

| 2021-01-01 12:00:00 |

NA |

NA |

NA |

NA |

NA |

| 2021-01-01 18:00:00 |

NA |

NA |

NA |

NA |

NA |

| 2021-01-02 00:00:00 |

29331.70 |

33300 |

28946.53 |

32178.33 |

129993.87 |

R

.grid <- df$time |>

lubridate::as_datetime() |>

(\(x) seq(min(x), max(x), by = "6 hours"))() |>

tibble::tibble(time = _)

.grid |>

left_join(df, by = "time") |>

head(5)

| 2021-01-01 00:00:00 |

28923.63 |

29600 |

28624.57 |

29331.69 |

54182.93 |

| 2021-01-01 06:00:00 |

NA |

NA |

NA |

NA |

NA |

| 2021-01-01 12:00:00 |

NA |

NA |

NA |

NA |

NA |

| 2021-01-01 18:00:00 |

NA |

NA |

NA |

NA |

NA |

| 2021-01-02 00:00:00 |

29331.70 |

33300 |

28946.53 |

32178.33 |

129993.87 |

Python

lf.collect().sort("time").upsample("time", every="6h").head(5)

shape: (5, 6)

| date |

f64 |

f64 |

f64 |

f64 |

f64 |

| 2021-01-01 |

28923.63 |

29600.0 |

28624.57 |

29331.69 |

54182.925011 |

| 2021-01-01 |

null |

null |

null |

null |

null |

| 2021-01-01 |

null |

null |

null |

null |

null |

| 2021-01-01 |

null |

null |

null |

null |

null |

| 2021-01-02 |

29331.7 |

33300.0 |

28946.53 |

32178.33 |

129993.873362 |

Window Functions

It is necessary to be careful how the Window function calculates if the

width of the window is less than the specified value.

Moving Average, Cumulative Avarage

PRQL has a dedicated way of applying the window to the entire table. For

the others, use a individual function for each column.

In R, base R have some window functions like cumsum, but none like

cumulative avarage. dplyr complements this with several functions,

including cummean.

Polars does not yet have a dedicated function to compute cumulative

averages, so we must use cumulative sums to compute them.

- PRQL DuckDB

- SQL DuckDB

- dplyr R

- Python Polars

PRQL

from tab

sort this.time

window rolling:28 (

derive {`28D MA` = average close}

)

window rows:..0 (

derive {`Expanding Average` = average close}

)

select {

this.time,

Raw = close,

`28D MA`,

`Expanding Average`

}

take 26..30

| 2021-01-26 |

32467.77 |

35032.87 |

35032.87 |

| 2021-01-27 |

30366.15 |

34860.03 |

34860.03 |

| 2021-01-28 |

33364.86 |

34806.63 |

34806.63 |

| 2021-01-29 |

34252.20 |

34982.36 |

34787.51 |

| 2021-01-30 |

34262.88 |

35056.81 |

34770.02 |

SQL

FROM tab

SELECT

time,

close AS "Raw",

avg(close) OVER (

ORDER BY time

ROWS BETWEEN 27 PRECEDING AND CURRENT ROW

) AS "28D MA",

avg(close) OVER (

ORDER BY time

ROWS BETWEEN UNBOUNDED PRECEDING AND CURRENT ROW

) AS "Expanding Average"

LIMIT 5 OFFSET 25

| 2021-01-26 |

32467.77 |

35032.87 |

35032.87 |

| 2021-01-27 |

30366.15 |

34860.03 |

34860.03 |

| 2021-01-28 |

33364.86 |

34806.63 |

34806.63 |

| 2021-01-29 |

34252.20 |

34982.36 |

34787.51 |

| 2021-01-30 |

34262.88 |

35056.81 |

34770.02 |

R

roll_and_expand <- df |>

arrange(time) |>

mutate(

time,

Raw = close,

`28D MA` = close |>

slider::slide_vec(mean, .before = 27, .complete = TRUE),

`Expanding Average` = cummean(close),

.keep = "none"

)

R

roll_and_expand |>

slice(26:30)

| 2021-01-26 |

32467.77 |

NA |

35032.87 |

| 2021-01-27 |

30366.15 |

NA |

34860.03 |

| 2021-01-28 |

33364.86 |

34806.63 |

34806.63 |

| 2021-01-29 |

34252.20 |

34982.36 |

34787.51 |

| 2021-01-30 |

34262.88 |

35056.81 |

34770.02 |

Python

close = pl.col("close")

roll_and_expand = lf.sort("time").select(

[

pl.col("time"),

close.alias("Raw"),

close.rolling_mean(28).alias("28D MA"),

close.alias("Expanding Average").cum_sum() / (close.cum_count() + 1),

]

)

Python

roll_and_expand.head(30).tail(5).collect()

shape: (5, 4)

| date |

f64 |

f64 |

f64 |

| 2021-01-26 |

32467.77 |

null |

33735.354074 |

| 2021-01-27 |

30366.15 |

null |

33615.025357 |

| 2021-01-28 |

33364.86 |

34806.6275 |

33606.398966 |

| 2021-01-29 |

34252.2 |

34982.36 |

33627.925667 |

| 2021-01-30 |

34262.88 |

35056.808214 |

33648.408065 |

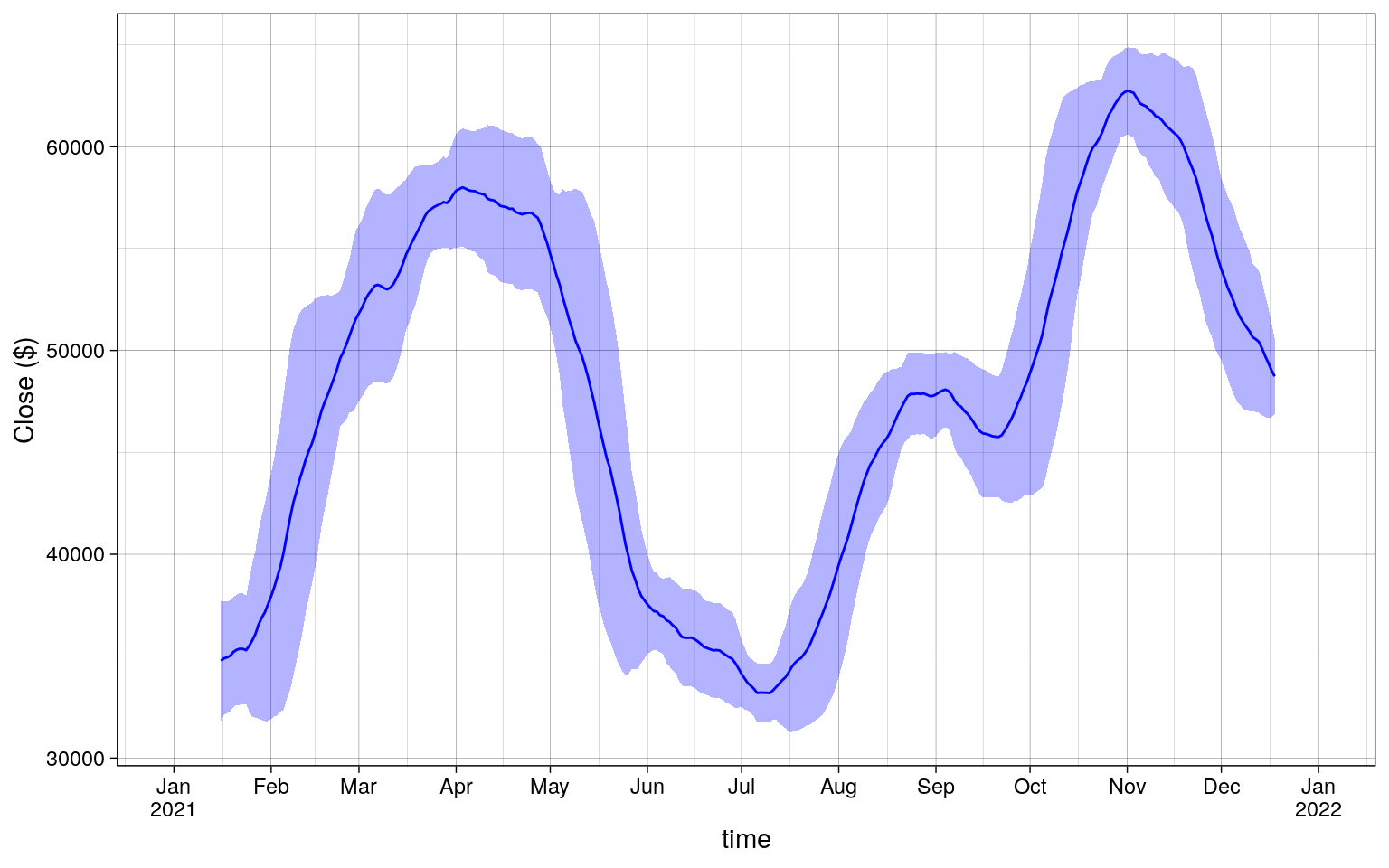

Here, DuckDB also calculates avarage for cases where the window width is

less than 28 for the 28D MA column, whereas R

slider::slide_vec(.complete = TRUE) and Polars rolling_mean make

them missing values. If we are using DuckDB and need to make replacement

for NULL, we need to add further processing.

Plotting the results of dplyr shows the following.

Code

R

library(ggplot2)

roll_and_expand |>

tidyr::pivot_longer(cols = !time) |>

ggplot(aes(time, value, colour = name)) +

geom_line() +

theme_linedraw() +

labs(y = "Close ($)") +

scale_x_date(

date_breaks = "month",

labels = scales::label_date_short()

)

Combining Rolling Aggregations

- PRQL DuckDB

- SQL DuckDB

- dplyr R

- Python Polars

PRQL

from tab

sort this.time

window rows:-15..14 (

select {

this.time,

mean = average close,

std = stddev close

}

)

take 13..17

| 2021-01-13 |

34860.03 |

3092.516 |

| 2021-01-14 |

34806.63 |

3047.833 |

| 2021-01-15 |

34787.51 |

2994.683 |

| 2021-01-16 |

34770.02 |

2944.156 |

| 2021-01-17 |

34895.40 |

2780.095 |

SQL

FROM tab

SELECT

time,

avg(close) OVER (

ORDER BY time

ROWS BETWEEN 15 PRECEDING AND 14 FOLLOWING

) AS mean,

stddev(close) OVER (

ORDER BY time

ROWS BETWEEN 15 PRECEDING AND 14 FOLLOWING

) AS std

ORDER BY time

LIMIT 5 OFFSET 12

| 2021-01-13 |

34860.03 |

3092.516 |

| 2021-01-14 |

34806.63 |

3047.833 |

| 2021-01-15 |

34787.51 |

2994.683 |

| 2021-01-16 |

34770.02 |

2944.156 |

| 2021-01-17 |

34895.40 |

2780.095 |

R

.slide_func <- function(.x, .fn) {

slider::slide_vec(.x, .fn, .before = 15, .after = 14, .complete = TRUE)

}

mean_std <- df |>

arrange(time) |>

mutate(

time,

across(

close,

.fns = list(mean = \(x) .slide_func(x, mean), std = \(x) .slide_func(x, sd)),

.names = "{.fn}"

),

.keep = "none"

)

| 2021-01-13 |

NA |

NA |

| 2021-01-14 |

NA |

NA |

| 2021-01-15 |

NA |

NA |

| 2021-01-16 |

34770.02 |

2944.156 |

| 2021-01-17 |

34895.40 |

2780.095 |

Python

mean_std = lf.sort("time").select(

time=pl.col("time"),

mean=pl.col("close").rolling_mean(30, center=True),

std=pl.col("close").rolling_std(30, center=True),

)

Python

mean_std.head(17).tail(5).collect()

shape: (5, 3)

| date |

f64 |

f64 |

| 2021-01-13 |

null |

null |

| 2021-01-14 |

null |

null |

| 2021-01-15 |

null |

null |

| 2021-01-16 |

34770.021667 |

2944.155675 |

| 2021-01-17 |

34895.398 |

2780.095304 |

As in Section 5.1,

here too the DuckDB results differ from the others.

Plotting the results of dplyr shows the following.

Code

R

library(ggplot2)

mean_std |>

ggplot(aes(time)) +

geom_ribbon(

aes(ymin = mean - std, ymax = mean + std),

alpha = 0.3, fill = "blue"

) +

geom_line(aes(y = mean), color = "blue") +

theme_linedraw() +

labs(y = "Close ($)") +

scale_x_date(

date_breaks = "month",

labels = scales::label_date_short()

)

Timezones

In DuckDB, the icu DuckDB extension is needed for time zones support. If

the DuckDB client that we are using does not contain the extension, we

need to install and load it.

- PRQL DuckDB

- SQL DuckDB

- dplyr R

- Python Polars

PRQL

let timezone = tz col -> s"timezone({tz}, {col})"

from tab

derive {

time_new = (this.time | timezone "UTC" | timezone "US/Eastern")

}

select !{this.time}

take 5

| 28923.63 |

29600.00 |

28624.57 |

29331.69 |

54182.93 |

2020-12-31 19:00:00 |

| 29331.70 |

33300.00 |

28946.53 |

32178.33 |

129993.87 |

2021-01-01 19:00:00 |

| 32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.57 |

2021-01-02 19:00:00 |

| 33000.05 |

33600.00 |

28130.00 |

31988.71 |

140899.89 |

2021-01-03 19:00:00 |

| 31989.75 |

34360.00 |

29900.00 |

33949.53 |

116050.00 |

2021-01-04 19:00:00 |

SQL

FROM tab

SELECT

* REPLACE timezone('US/Eastern', timezone('UTC', time)) AS time

LIMIT 5

| 2020-12-31 19:00:00 |

28923.63 |

29600.00 |

28624.57 |

29331.69 |

54182.93 |

| 2021-01-01 19:00:00 |

29331.70 |

33300.00 |

28946.53 |

32178.33 |

129993.87 |

| 2021-01-02 19:00:00 |

32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.57 |

| 2021-01-03 19:00:00 |

33000.05 |

33600.00 |

28130.00 |

31988.71 |

140899.89 |

| 2021-01-04 19:00:00 |

31989.75 |

34360.00 |

29900.00 |

33949.53 |

116050.00 |

R

df |>

mutate(

time = time |>

lubridate::force_tz("UTC") |>

lubridate::with_tz("US/Eastern")

) |>

head(5)

| 2020-12-31 19:00:00 |

28923.63 |

29600.00 |

28624.57 |

29331.69 |

54182.93 |

| 2021-01-01 19:00:00 |

29331.70 |

33300.00 |

28946.53 |

32178.33 |

129993.87 |

| 2021-01-02 19:00:00 |

32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.57 |

| 2021-01-03 19:00:00 |

33000.05 |

33600.00 |

28130.00 |

31988.71 |

140899.89 |

| 2021-01-04 19:00:00 |

31989.75 |

34360.00 |

29900.00 |

33949.53 |

116050.00 |

Python

(

lf.with_columns(

pl.col("time")

.cast(pl.Datetime)

.dt.replace_time_zone("UTC")

.dt.convert_time_zone("US/Eastern")

)

.head(5)

.collect()

)

shape: (5, 6)

| datetime[μs, US/Eastern] |

f64 |

f64 |

f64 |

f64 |

f64 |

| 2020-12-31 19:00:00 EST |

28923.63 |

29600.0 |

28624.57 |

29331.69 |

54182.925011 |

| 2021-01-01 19:00:00 EST |

29331.7 |

33300.0 |

28946.53 |

32178.33 |

129993.873362 |

| 2021-01-02 19:00:00 EST |

32176.45 |

34778.11 |

31962.99 |

33000.05 |

120957.56675 |

| 2021-01-03 19:00:00 EST |

33000.05 |

33600.0 |

28130.0 |

31988.71 |

140899.88569 |

| 2021-01-04 19:00:00 EST |

31989.75 |

34360.0 |

29900.0 |

33949.53 |

116049.997038 |

Note that each system may keep time zone information in a different way.

Here, the time column (and the time_new column) in DuckDB results

are the TIMESTAMP type, has no time zone information.